Looking to buy?

Having the right guidance can make the process far less stressful. Below is a complete home buying checklist that covers everything you need to know, including budgeting, saving a deposit, home loan preparation, property inspections, government grants, key questions to ask, and important financial considerations.

Learn how to buy a home with confidence, avoid common mistakes, and make smarter property decisions.

Book a call with Nexus Loans today and get expert guidance tailored to your goals.

Home buying checklist

Buying a home is exciting, but there’s a lot to consider before making an offer. This checklist is designed to help you stay organised, ask the right questions, and feel confident throughout the buying process. From budgeting and inspections to finance, location, and future growth, these are the key things every buyer should look for before purchasing a property.

Builder and Developer Reputation

If you’re buying a newly built home or off-the-plan property, research the builder or developer carefully. Review previous projects, customer feedback, build quality, and reputation within the industry to help reduce the risk of delays, defects, or poor workmanship.

Taking the time to research before buying can help you make a more informed property decision and feel confident moving forward with your home purchase journey.

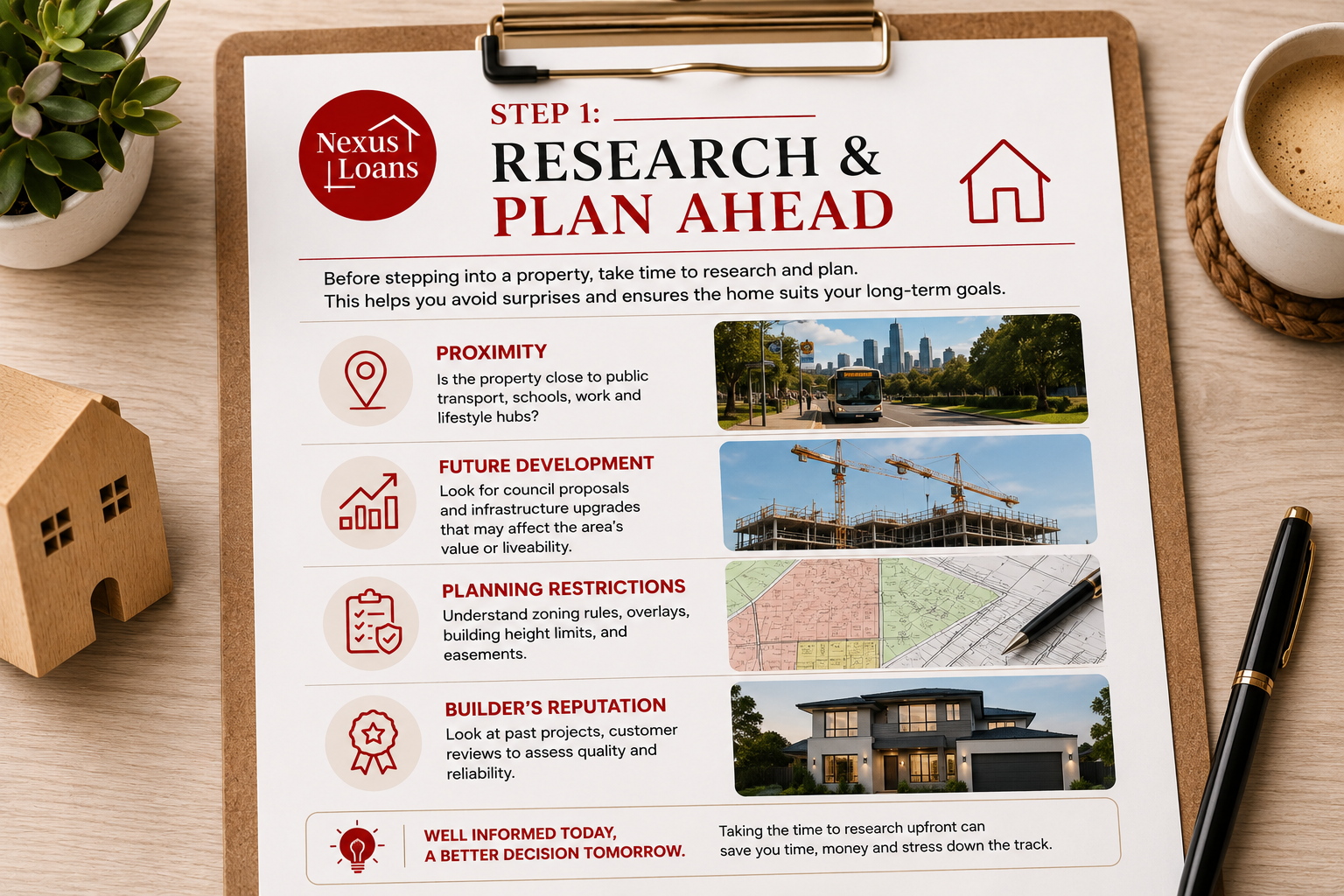

Step 1:

Research and Plan Ahead

Buying a home is one of the biggest financial decisions you’ll make, so taking the time to research the property and surrounding area before you buy is essential. Proper planning can help you avoid costly mistakes, identify future growth opportunities, and ensure the property suits your lifestyle and long-term goals.

Proximity to Essential Amenities

Consider how close the property is to public transport, schools, shopping centres, healthcare services, cafes, parks, and your workplace. A well-located home can improve your lifestyle, increase convenience, and support stronger property value growth over time.

Future Development and Growth

Research planned infrastructure projects, new developments, and council upgrades in the area. Future roads, schools, transport links, shopping precincts, and community facilities can significantly impact property values, traffic, noise levels, and overall liveability.

Planning Restrictions and Zoning

Before purchasing, understand local council zoning, overlays, easements, and building restrictions that may affect the property. These can influence future renovations, extensions, subdivision opportunities, and the long-term potential of the home.

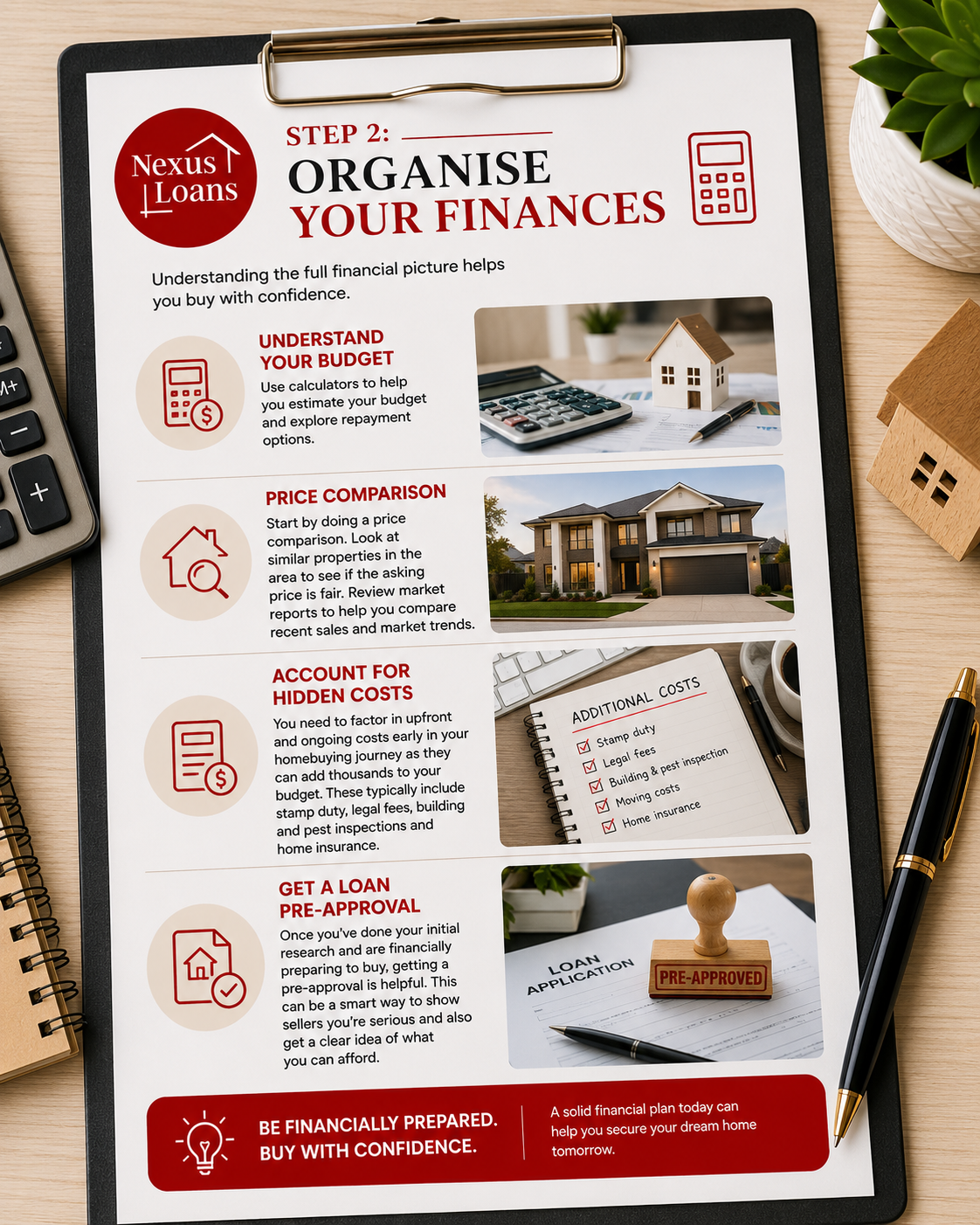

Get a Home Loan Pre-Approval

A home loan pre-approval gives you a clearer understanding of your borrowing capacity and helps you shop for property with confidence. It can also strengthen your position when making an offer, as sellers and real estate agents can see you’re financially prepared and serious about buying.

Getting financially organised early can help you avoid delays, reduce stress, and put you in a stronger position when it’s time to purchase your home.

Step 2:

Organise Your Finances

Getting your finances organised is one of the most important steps when buying a home. Understanding your borrowing power, budgeting correctly, and preparing for upfront costs can help make the home buying process smoother and less stressful.

Understand Your Budget and Borrowing Power

Before searching for a property, it’s important to understand how much you can realistically afford. Use home loan calculators to estimate your borrowing capacity, compare repayment options, and create a budget that suits your lifestyle and financial goals.

Compare Property Prices and Market TrendS

Research similar properties in the area to determine whether a property is priced fairly. Reviewing recent sales, suburb growth trends, and local market reports can help you make informed decisions and avoid overpaying.

Plan for Upfront and Ongoing Costs

Buying a property involves more than just the purchase price. Make sure you budget for additional costs such as:

Stamp duty

Conveyancing and legal fees

Building and pest inspections

Loan application fees

Moving expenses

Home and contents insurance

These costs can add thousands to your overall budget, so planning ahead is essential.

Evaluate the Layout and Functionality

Consider Noise, Privacy, and Surroundings

Inspect the surrounding area and assess traffic noise, neighbouring properties, privacy, and nearby amenities. Visiting the property at different times of the day can help you better understand the neighbourhood and environment.

Carefully inspecting a property before buying can help you avoid hidden problems and make a more informed home buying decision.

Step 3:

What to Look for During a House Inspection

A property inspection is your chance to look beyond the styling and presentation of a home. Taking the time to properly inspect the property can help you identify potential issues, understand the home’s condition, and decide whether it suits your lifestyle and long-term goals.

Check the Structural Condition

Look for signs of structural damage such as cracks in walls, uneven floors, water stains, damp patches, mould, or ceiling movement. These can indicate underlying building issues that may lead to costly repairs in the future.

Assess Natural Light and Ventilation

Pay attention to natural light, airflow, window placement, and the overall orientation of the home. A bright, well-ventilated property can improve comfort, energy efficiency, and liveability.

Walk through the property and think about how the space will work for your daily lifestyle. Consider room sizes, storage, accessibility, parking, outdoor space, and whether the layout suits your current and future needs.

Identify Environmental or Legal Restrictions

Check whether the property is affected by bushfire zones, flood overlays, heritage listings, easements, or other restrictions that could impact insurance, future renovations, or property value.

The more questions you ask before purchasing, the more confident and informed you’ll feel when making one of the biggest financial decisions of your life.

Step 4:

Questions to Ask During a House Inspection

Asking the right questions during a property inspection can uncover important details that may not be immediately visible. Speaking with the real estate agent, reviewing documentation, and seeking legal advice can help you better understand the property before making an offer.

Ask About Known Issues or Repairs

Find out whether the property has had any recent repairs, water damage, structural issues, pest problems, or ongoing maintenance concerns. Understanding the property’s history can help you identify potential risks.

Understand Council Rates and Ongoing Costs

Ask about council rates, strata fees, utilities, and other ongoing expenses associated with the property. Knowing these costs early can help you plan your budget more accurately.

Check Renovation or Extension Restrictions

If you plan to renovate, extend, subdivide, or make changes to the property, ask about council regulations, zoning restrictions, easements, and permits that may affect future plans.

First Home Super Saver Scheme (FHSS)

The First Home Super Saver Scheme allows eligible buyers to use voluntary superannuation contributions to help save for a home deposit. This strategy may offer tax advantages while helping you build savings faster.

Understanding available first home buyer grants and government assistance programs can help you save money, increase your borrowing options, and achieve your home ownership goals sooner.

Government Schemes for First Home Buyers

f you’re buying your first home, there are a range of government grants and first home buyer schemes that may help reduce upfront costs, boost your deposit, and make home ownership more accessible. Eligibility criteria and benefits can vary depending on your income, location, and the property you’re purchasing, so it’s important to understand which options may apply to you.

First Home Owner Grant (FHOG)

The First Home Owner Grant is a one-off government payment available to eligible first home buyers purchasing or building a new home. Grant amounts and eligibility requirements vary between states and territories.

Stamp Duty Concessions

Many first home buyers may qualify for reduced or waived stamp duty depending on the property value and the state they’re buying in. Stamp duty concessions can potentially save buyers thousands of dollars in upfront costs.

Australian Government 5% Deposit Scheme

Eligible first home buyers may be able to purchase a property with as little as a 5% deposit without paying Lenders Mortgage Insurance (LMI). Some schemes also allow eligible single parents to buy with only a 2% deposit, helping more Australians enter the property market sooner.

Access to multiple lenders

We have access to multiple lenders through our network. Unlike loan officers tied to a single institution, We can compare offers from various lenders, providing borrowers with a range of options to find the best terms and rates for their needs.

Our relationship doesn’t end once you secure your mortgage; we pride ourselves on maintaining a lasting partnership. We offer ongoing mortgage health checks throughout the life of your loan, ensuring that you always have the best service, product, and structure to suit your evolving financial needs.

Book a call with Jessie today

Curious about what you can afford? Our free mortgage calculators make it easy to estimate your borrowing capacity, repayments, and property fees. Try them out and get a clearer picture of your next move before you apply.

Calculators

Loans That Make Sence

-

Want to Invest

Investing in real estate can be a great way to build wealth over the long term.

-

Unique Loans

Looking to renovate or build?

We help you find the right loan for your situation. -

Refinance and Save

Refinancing is a powerful financial tool that can save you money.